Black Box AI in Treasury: The Risks CFOs and Treasurers Can't Ignore

AI adoption in treasury is accelerating. The solutions on the market range from genuinely useful to genuinely risky, and the difference often comes down to one question: can you explain how the AI arrived at its recommendation?

For treasury teams, that question is not abstract. It has direct implications for board accountability, audit readiness and the confidence with which you can act on AI-generated outputs.

The EU AI Act, which began phasing in 2025 and brings full obligations for high-risk financial AI by August 2026, now mandates traceability logs and human oversight procedures for AI systems that influence financial outcomes. The regulatory direction of travel is clear, regardless of jurisdiction.

This page explains what black box AI is, why it creates real risk in a treasury context and what transparent AI looks like in practice.

For a broader view of how AI fits into treasury operations, see our AI treasury management guide. When you're ready to apply these principles to vendor selection, see our guide to how to evaluate AI treasury software.

What Is Black Box AI?

Black box AI refers to any system that produces outputs, recommendations, predictions, alerts, without providing a traceable explanation of how it arrived at them. The model processes inputs and returns a result, but the reasoning that connects the two is opaque.

This is a common characteristic of certain machine learning architectures, particularly deep neural networks, where the internal logic is distributed across millions of parameters in ways that resist simple interpretation. The model may be highly accurate on average, but for any individual output, the path from input to conclusion is not visible.

In treasury, that trade-off is not acceptable.

Why Black Box AI Is a Problem for Treasury

Treasury operates under a set of accountability requirements that most business functions don't face in the same way. Cash positioning decisions affect the organization's ability to meet obligations. Liquidity recommendations inform capital allocation. Forecast assumptions flow into board presentations and investor communications.

When a recommendation influences a decision at that level, someone needs to be able to explain it. That means the treasury professional presenting to the board, the internal auditor reviewing the decision trail and, in regulated environments, the external examiner asking why a particular action was taken.

Black box AI creates several distinct risks in this context:

- Unexplainable recommendations. If the AI flags a liquidity risk or recommends a funding action and you cannot trace that recommendation to specific data, you cannot defend it. A CFO presenting a major decision based on an algorithm they cannot explain is in a difficult position with any informed audience.

- Undetectable errors. When AI reasoning is opaque, errors in logic or data are harder to catch. A transparent system lets you review the inputs and the reasoning. An opaque one requires you to trust the output without the ability to verify it.

- Audit exposure. Finance functions are subject to internal and external audit. AI-influenced decisions need to be explainable in retrospect, often months or years after the fact. Black box systems frequently cannot provide that trail, and regulators are now specifically looking for it. The PCAOB's 2025 inspection priorities explicitly called out the explainability of AI models and AI-influenced financial outputs as an area of examiner focus. "The platform calculated it" is not a sufficient response to an auditor's question about a cash positioning decision.

- Regulatory risk. Financial services regulators have moved from general concern to specific guidance. In March 2026, the U.S. Department of the Treasury released the Financial Services AI Risk Management Framework (FS AI RMF), with 230 control objectives covering AI transparency across the full AI lifecycle. While currently voluntary, the framework is expected to shape auditor standards as adoption accelerates. Using black box AI in treasury is increasingly a compliance readiness question.

- Erosion of trust. When treasury teams cannot explain AI outputs to leadership, adoption stalls. The solution that was supposed to improve decision-making becomes a liability because no one is comfortable acting on recommendations they cannot interrogate.

What Transparent AI Looks Like in Treasury

Transparent AI provides a complete, auditable explanation for every output. That means the reasoning is traceable, human-readable and accessible when you need it.

Consider the difference between a black-box output and a transparent one:

- Black box: "Forecast: $4.2M"

- Transparent: "Forecast: $4.2M. Driven by 12% reduction in AR collections from Entity 3, seasonal dip in customer payment timing, offset by $800K intercompany settlement expected Thursday"

The CFA Institute's 2025 report on Explainable AI in Finance found that explainability needs vary by stakeholder — boards require strategic clarity, auditors require traceable logic, and operators require actionable specificity. Transparent treasury AI should satisfy all three simultaneously. The number is the same. The second gives your team something to act on, verify, and explain to each audience.

The number is the same. The second gives your team something to act on, verify, and explain to stakeholders.

In practice, transparent treasury AI should provide:

- Audit trails that link every recommendation to the specific data points that informed it, with enough detail to reconstruct the reasoning months after the fact

- Customer data isolation ensuring that insights generated for your organization are based exclusively on your data, never mixed with other clients

- Plain-language explanations that a CFO can present to a board without needing a data scientist to translate

- Explainable variance narratives that identify which specific transactions, customers or categories drove the change and why it matters

- Versioning and logging so that recommendations made at a point in time can be reviewed and explained later

This level of transparency is achievable. It requires deliberate architectural decisions on the part of the AI provider, which is why it varies so significantly across solutions currently on the market.

Questions to Ask Any AI Vendor

Evaluating AI transparency requires asking direct questions before you commit to a solution. Vague answers or references to proprietary algorithms that can't be explained are significant warning signs.

Ask every vendor you evaluate:

- Can you show me an audit trail for a specific recommendation, from output back to source data?

- How does your system handle situations where the data inputs were incorrect or incomplete? Is that visible after the fact?

- Is my organization's data processed in isolation, or does it interact with data from other clients in any way?

- Can your system's recommendations be explained to a non-technical audience, such as a board or audit committee?

- How would you help us respond to an auditor asking why the AI made a specific recommendation six months ago?

- Does my data train your models? If so, how?

The answers to these questions reveal more about whether an AI solution is appropriate for treasury use than any feature comparison.

The Connection Between Transparency and Adoption

There is a practical reason to prioritize transparency beyond compliance and audit readiness. Treasury teams that cannot explain AI outputs to leadership don't use them confidently, and AI that isn't used confidently doesn't deliver value.

The organizations getting the most from treasury AI are the ones where the team trusts the outputs enough to act on them. That trust is built through transparency. When an analyst can see exactly why the AI flagged a variance, trace a liquidity recommendation back to the underlying cash position data and present a board-ready narrative with confidence in its accuracy, AI becomes a genuine tool rather than a liability.

Explainability is what converts AI capability into treasury value.

What to Look for in Transparent Treasury AI

When evaluating solutions, these are the characteristics that distinguish genuinely transparent AI from systems that use "explainability" as a marketing term:

- Source-data traceability. Every output links to specific inputs rather than a summary of inputs.

- Client data isolation. Your data never influences recommendations generated for another organization.

- Human-readable reasoning. Explanations are written in plain language appropriate for a finance audience, not technical output requiring interpretation.

- Retrospective accessibility. Audit trails are accessible and meaningful months or years after a recommendation was made.

- Inference-only architecture. Your data is used to generate insights, not to train models that serve other clients.

If a vendor cannot demonstrate all of these characteristics with specific examples, that gap warrants serious scrutiny before you proceed.

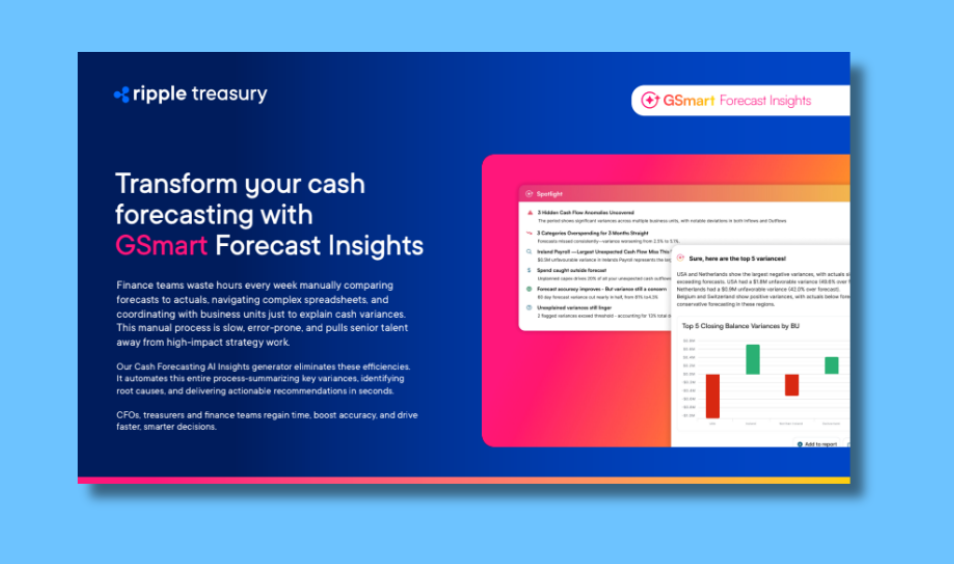

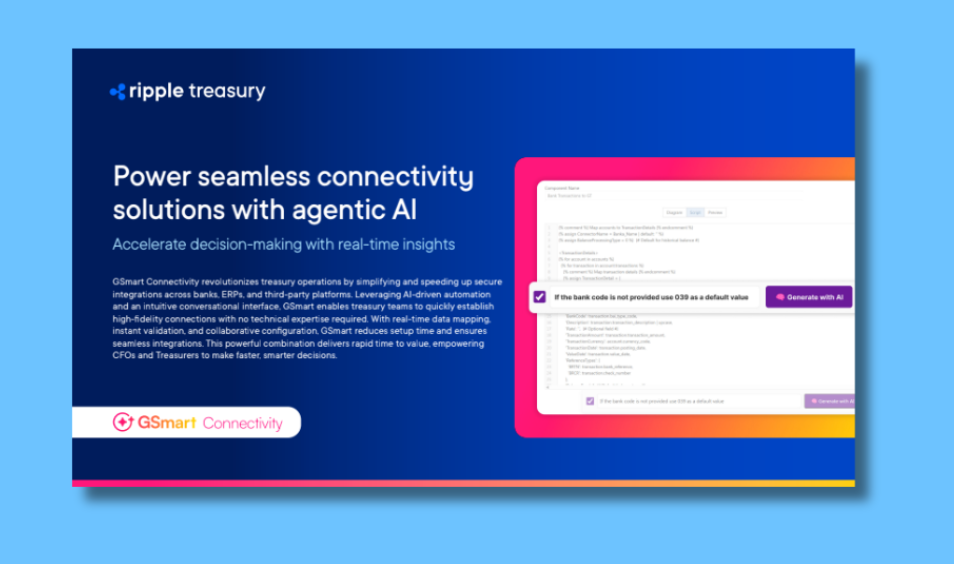

GSmart AI by Ripple Treasury

Ripple Treasury built GSmart AI around a foundational commitment to transparency that addresses each of the risks described above.

Every GSmart AI recommendation comes with a full audit trail traceable to the specific data points that informed it. Each customer's data is processed in complete isolation, insights generated for your organization are never mixed with data from other clients. GSmart AI uses inference-only architecture, meaning your data generates insights for you and does not train models that serve anyone else.

The outputs are written in plain language appropriate for board and executive audiences. Variance narratives, liquidity alerts and forecast explanations are designed to be presented directly to leadership without requiring translation or qualification.

This approach is not incidental to how GSmart AI works. It is the design principle the system was built around, because Ripple Treasury understands that AI treasury teams cannot explain is AI they cannot use.

To see how GSmart AI delivers transparent, auditable results for treasury operations, visit the GSmart AI solution page.

Frequently Asked Questions

What is black box AI?

Black box AI refers to systems that produce outputs without providing a traceable explanation of how they arrived at them. The reasoning that connects inputs to recommendations is opaque, making it difficult or impossible to audit, explain or verify individual outputs.

Why is black box AI risky for treasury?

Treasury decisions affect cash positioning, liquidity and capital allocation at an organizational level. When those decisions are influenced by AI recommendations, the reasoning behind them must be explainable to boards, auditors and regulators. Black box AI cannot provide that explanation, creating audit exposure, regulatory risk and erosion of trust in AI outputs.

What does explainable AI mean in a treasury context?

Explainable AI in treasury means every recommendation comes with an audit trail linking it to specific source data, expressed in plain language that a finance audience can understand and review. It also means client data isolation, retrospective accessibility and inference-only architecture that prevents your data from training models used by other organizations.

How can I tell if an AI vendor's explainability claims are genuine?

Ask for a live demonstration of an audit trail for a specific recommendation, from output back to source data. Ask whether your data trains their models. Ask how they would help you respond to an auditor's question about a recommendation made six months ago. Genuine transparency is demonstrable. Vendors who cannot demonstrate it specifically are unlikely to deliver it in production.

Black Box AI in Treasury: The Risks CFOs and Treasurers Can't Ignore

AI adoption in treasury is accelerating. The solutions on the market range from genuinely useful to genuinely risky, and the difference often comes down to one question: can you explain how the AI arrived at its recommendation?

For treasury teams, that question is not abstract. It has direct implications for board accountability, audit readiness and the confidence with which you can act on AI-generated outputs.

The EU AI Act, which began phasing in 2025 and brings full obligations for high-risk financial AI by August 2026, now mandates traceability logs and human oversight procedures for AI systems that influence financial outcomes. The regulatory direction of travel is clear, regardless of jurisdiction.

This page explains what black box AI is, why it creates real risk in a treasury context and what transparent AI looks like in practice.

For a broader view of how AI fits into treasury operations, see our AI treasury management guide. When you're ready to apply these principles to vendor selection, see our guide to how to evaluate AI treasury software.

What Is Black Box AI?

Black box AI refers to any system that produces outputs, recommendations, predictions, alerts, without providing a traceable explanation of how it arrived at them. The model processes inputs and returns a result, but the reasoning that connects the two is opaque.

This is a common characteristic of certain machine learning architectures, particularly deep neural networks, where the internal logic is distributed across millions of parameters in ways that resist simple interpretation. The model may be highly accurate on average, but for any individual output, the path from input to conclusion is not visible.

In treasury, that trade-off is not acceptable.

Why Black Box AI Is a Problem for Treasury

Treasury operates under a set of accountability requirements that most business functions don't face in the same way. Cash positioning decisions affect the organization's ability to meet obligations. Liquidity recommendations inform capital allocation. Forecast assumptions flow into board presentations and investor communications.

When a recommendation influences a decision at that level, someone needs to be able to explain it. That means the treasury professional presenting to the board, the internal auditor reviewing the decision trail and, in regulated environments, the external examiner asking why a particular action was taken.

Black box AI creates several distinct risks in this context:

- Unexplainable recommendations. If the AI flags a liquidity risk or recommends a funding action and you cannot trace that recommendation to specific data, you cannot defend it. A CFO presenting a major decision based on an algorithm they cannot explain is in a difficult position with any informed audience.

- Undetectable errors. When AI reasoning is opaque, errors in logic or data are harder to catch. A transparent system lets you review the inputs and the reasoning. An opaque one requires you to trust the output without the ability to verify it.

- Audit exposure. Finance functions are subject to internal and external audit. AI-influenced decisions need to be explainable in retrospect, often months or years after the fact. Black box systems frequently cannot provide that trail, and regulators are now specifically looking for it. The PCAOB's 2025 inspection priorities explicitly called out the explainability of AI models and AI-influenced financial outputs as an area of examiner focus. "The platform calculated it" is not a sufficient response to an auditor's question about a cash positioning decision.

- Regulatory risk. Financial services regulators have moved from general concern to specific guidance. In March 2026, the U.S. Department of the Treasury released the Financial Services AI Risk Management Framework (FS AI RMF), with 230 control objectives covering AI transparency across the full AI lifecycle. While currently voluntary, the framework is expected to shape auditor standards as adoption accelerates. Using black box AI in treasury is increasingly a compliance readiness question.

- Erosion of trust. When treasury teams cannot explain AI outputs to leadership, adoption stalls. The solution that was supposed to improve decision-making becomes a liability because no one is comfortable acting on recommendations they cannot interrogate.

What Transparent AI Looks Like in Treasury

Transparent AI provides a complete, auditable explanation for every output. That means the reasoning is traceable, human-readable and accessible when you need it.

Consider the difference between a black-box output and a transparent one:

- Black box: "Forecast: $4.2M"

- Transparent: "Forecast: $4.2M. Driven by 12% reduction in AR collections from Entity 3, seasonal dip in customer payment timing, offset by $800K intercompany settlement expected Thursday"

The CFA Institute's 2025 report on Explainable AI in Finance found that explainability needs vary by stakeholder — boards require strategic clarity, auditors require traceable logic, and operators require actionable specificity. Transparent treasury AI should satisfy all three simultaneously. The number is the same. The second gives your team something to act on, verify, and explain to each audience.

The number is the same. The second gives your team something to act on, verify, and explain to stakeholders.

In practice, transparent treasury AI should provide:

- Audit trails that link every recommendation to the specific data points that informed it, with enough detail to reconstruct the reasoning months after the fact

- Customer data isolation ensuring that insights generated for your organization are based exclusively on your data, never mixed with other clients

- Plain-language explanations that a CFO can present to a board without needing a data scientist to translate

- Explainable variance narratives that identify which specific transactions, customers or categories drove the change and why it matters

- Versioning and logging so that recommendations made at a point in time can be reviewed and explained later

This level of transparency is achievable. It requires deliberate architectural decisions on the part of the AI provider, which is why it varies so significantly across solutions currently on the market.

Questions to Ask Any AI Vendor

Evaluating AI transparency requires asking direct questions before you commit to a solution. Vague answers or references to proprietary algorithms that can't be explained are significant warning signs.

Ask every vendor you evaluate:

- Can you show me an audit trail for a specific recommendation, from output back to source data?

- How does your system handle situations where the data inputs were incorrect or incomplete? Is that visible after the fact?

- Is my organization's data processed in isolation, or does it interact with data from other clients in any way?

- Can your system's recommendations be explained to a non-technical audience, such as a board or audit committee?

- How would you help us respond to an auditor asking why the AI made a specific recommendation six months ago?

- Does my data train your models? If so, how?

The answers to these questions reveal more about whether an AI solution is appropriate for treasury use than any feature comparison.

The Connection Between Transparency and Adoption

There is a practical reason to prioritize transparency beyond compliance and audit readiness. Treasury teams that cannot explain AI outputs to leadership don't use them confidently, and AI that isn't used confidently doesn't deliver value.

The organizations getting the most from treasury AI are the ones where the team trusts the outputs enough to act on them. That trust is built through transparency. When an analyst can see exactly why the AI flagged a variance, trace a liquidity recommendation back to the underlying cash position data and present a board-ready narrative with confidence in its accuracy, AI becomes a genuine tool rather than a liability.

Explainability is what converts AI capability into treasury value.

What to Look for in Transparent Treasury AI

When evaluating solutions, these are the characteristics that distinguish genuinely transparent AI from systems that use "explainability" as a marketing term:

- Source-data traceability. Every output links to specific inputs rather than a summary of inputs.

- Client data isolation. Your data never influences recommendations generated for another organization.

- Human-readable reasoning. Explanations are written in plain language appropriate for a finance audience, not technical output requiring interpretation.

- Retrospective accessibility. Audit trails are accessible and meaningful months or years after a recommendation was made.

- Inference-only architecture. Your data is used to generate insights, not to train models that serve other clients.

If a vendor cannot demonstrate all of these characteristics with specific examples, that gap warrants serious scrutiny before you proceed.

GSmart AI by Ripple Treasury

Ripple Treasury built GSmart AI around a foundational commitment to transparency that addresses each of the risks described above.

Every GSmart AI recommendation comes with a full audit trail traceable to the specific data points that informed it. Each customer's data is processed in complete isolation, insights generated for your organization are never mixed with data from other clients. GSmart AI uses inference-only architecture, meaning your data generates insights for you and does not train models that serve anyone else.

The outputs are written in plain language appropriate for board and executive audiences. Variance narratives, liquidity alerts and forecast explanations are designed to be presented directly to leadership without requiring translation or qualification.

This approach is not incidental to how GSmart AI works. It is the design principle the system was built around, because Ripple Treasury understands that AI treasury teams cannot explain is AI they cannot use.

To see how GSmart AI delivers transparent, auditable results for treasury operations, visit the GSmart AI solution page.

Frequently Asked Questions

What is black box AI?

Black box AI refers to systems that produce outputs without providing a traceable explanation of how they arrived at them. The reasoning that connects inputs to recommendations is opaque, making it difficult or impossible to audit, explain or verify individual outputs.

Why is black box AI risky for treasury?

Treasury decisions affect cash positioning, liquidity and capital allocation at an organizational level. When those decisions are influenced by AI recommendations, the reasoning behind them must be explainable to boards, auditors and regulators. Black box AI cannot provide that explanation, creating audit exposure, regulatory risk and erosion of trust in AI outputs.

What does explainable AI mean in a treasury context?

Explainable AI in treasury means every recommendation comes with an audit trail linking it to specific source data, expressed in plain language that a finance audience can understand and review. It also means client data isolation, retrospective accessibility and inference-only architecture that prevents your data from training models used by other organizations.

How can I tell if an AI vendor's explainability claims are genuine?

Ask for a live demonstration of an audit trail for a specific recommendation, from output back to source data. Ask whether your data trains their models. Ask how they would help you respond to an auditor's question about a recommendation made six months ago. Genuine transparency is demonstrable. Vendors who cannot demonstrate it specifically are unlikely to deliver it in production.

Featured Resources

.png)

%404x.png)

See Ripple Treasury

in Action

Get connected with supportive experts, comprehensive solutions, and untapped possibility today.